An integral part of the formula to successfully buying a home is securing the correct amount of financing. Once you’ve found the home you’d like to pursue, one of your primary tasks is exploring different loan products to see which best fits your situation. Eventually, you’ll come to a fork in the road where you’ll need to decide between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). The following information will help you gain a better understanding of ARMs to help you decide whether they’re right for you.

What Is an Adjustable-Rate Mortgage (ARM)?

After your down payment, your mortgage will finance the remainder of your home purchase. Whereas fixed-rate mortgages allow you to lock in a specific interest rate and payment for the life of your loan, adjustable-rate mortgages’ interest rates will fluctuate over time, thus changing your loan payment. It’s typical for ARMs to begin with a low introductory interest rate, but once that first stage of the loan has passed, they will begin to shift up and down. ARMs generally have a cap that specifies the maximum rate that can occur for that loan.

Let’s say you secure an adjustable-rate mortgage with 30-year terms, the first five of which are at a fixed rate. When the variable interest portion of the loan kicks in, your mortgage’s fluctuations will be measured against an index. If the index is higher than when you secured the loan, your rate and loan payment will go up—and vice versa. How often your ARM rates change depends on your agreement with your lender. Talk to your mortgage broker to learn more about the characteristics of adjustable-rate mortgages.

Different Types of Adjustable-Rate Mortgages (ARMs)

Payment-Option ARM: You’ll have flexibility to choose your monthly payments with a payment-option ARM, including interest-only payments and minimum payments that don’t cover interest. These loan products can get home buyers into hot water quickly when rates increase.

Interest-Only ARM: With an interest-only ARM, you pay just the interest on the loan for a specified introductory period, then the principal payments kick in on top. The longer the introductory period, the higher your payments will be when the delayed principal payments enter the equation.

Hybrid ARM: As outlined above, a hybrid ARM begins with a fixed-rate introductory period followed by an adjustable-rate period. Typically, a hybrid ARM’s fixed-rate period lasts anywhere between three to 10 years, and its rates adjust at an agreed-upon frequency during the adjustable-rate period, such as once every six months or once a year.

Pros and Cons of an Adjustable-Rate Mortgage (ARM)

- The low introductory rate allows you to save money and plan for when the adjustable-rate period kicks in.

- If you plan to live in the home for a long time, a fixed-rate mortgage may be a better option.

- If you plan on selling in a few years, you can use the proceeds to pay back your mortgage before the fixed-rate period ends.

- Without knowing what will happen to interest rates, your monthly payments could become unaffordable.

- The low introductory rate allows you to save money and plan for when the adjustable-rate period kicks in.

- If you plan to live in the home for a long time, a fixed-rate mortgage may be a better option.

- If you plan on selling in a few years, you can use the proceeds to pay back your mortgage before the fixed-rate period ends.

- Without knowing what will happen to interest rates, your monthly payments could become unaffordable.

- If the index decreases over time, you could end up with a lower interest rate and monthly payments.

- Financial planning is more difficult with an ARM, since there’s no telling what your monthly payments will be one year to the next.

Home Monthly Payment Calculator

To get an idea of how your mortgage payment will fit into your budget, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price.

For more information on financing your next home purchase, connect with an experienced, local Windermere agent.

Featured Image Source: Getty Images – Image Credit: Pekic

We talk a lot about why it makes financial sense to buy a home, but more often than not, we’re drawn to the emotional reasons for homeownership.

No matter the living space, the feeling of a home means different things to different people. Whether it’s a certain scent or a favorite chair, the feel-good connections to our own homes are typically more important to us than the financial ones. Here are some of the reasons why.

1. Owning your home is an accomplishment worth celebrating

You’ve likely worked very hard to achieve this dream, and whether it’s your first home or your fifth, congratulations are in order for this milestone. You’ve earned it.

2. There’s no place like home

Owning your own home offers not only safety and security but also a comfortable place where you can simply relax and kick-back after a long day. Sometimes, that’s just what we need to feel recharged and truly content.

3. You can find more space to meet your needs

Whether you want more room in your home for your changing lifestyle (think: working from home, virtual school, or a personal gym), or you simply prefer to have a large backyard for socially-distant entertaining, you can invest in a location that truly works for your evolving needs.

4. You have control over renovations, updates, and your style

Looking to try one of those complicated wall treatments you saw on Pinterest? Tired of paying an additional pet deposit for your apartment building? Maybe you want to finally adopt that fur-baby puppy or kitten you’ve been hoping for. You can do all of these things in your own home.

Bottom Line

Whether you’re a first-time homebuyer or a move-up buyer who wants to start a new chapter in your life, now is a great time to reflect on the intangible factors that turn a house into a happy home.

The COVID-19 pandemic has affected populations across the globe, but those who struggle with poverty and count on food programs to meet their basic day-to-day needs are in an especially uncertain place. While coping with increased demand and a bottlenecked pipeline of food supply, food banks are desperate for funds to continue to serve their communities. Because of this, Windermere decided to challenge its offices to raise $250,000, every dollar of which would be matched by the Windermere Foundation and donated to food banks in the areas where Windermere operates. We titled it the “Neighbors in Need” fundraising campaign.

Neighbors in Need kicked off on April 21, with the goal of raising $250,000 by May 5. As word continued to spread, online donations and contributions from both our agents and the public began to increase. Neighbors in Need was given a boost by Seattle Seahawks starting safety Quandre Diggs in a heartfelt message encouraging support. Over the final 24 hours, leading up to the May 5 deadline, support poured in from across the Windermere family as the final figure exceeded the initial goal of $500,000, landing at a total of $690,000.

Neighbors in Need exemplifies Windermere’s deep commitment to supporting our local communities, which traces back to 1989 when the Windermere Foundation first started. Since then, we’ve proudly raised more than $41 million for low-income and homeless families throughout the Western U.S.

On behalf of the Windermere Foundation to all those who joined the effort: Thank you. We could not have made this large of an impact without your help. We are humbled to be able to do our part to help those who need it most during these uncertain times.

This post originally appeared on the Windermere.com Blog

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist, Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact me.

ECONOMIC OVERVIEW

Employment in Washington State continues to soften; it is currently at an annual growth rate of 1.7%. I believe that is a temporary slowdown and we will see the pace of employment growth improve as we move further into the new year. It’s clear that businesses are continuing to feel the effects of the trade war with China and this is impacting hiring practices. This is, of course, in addition to the issues that Boeing currently faces regarding the 737 MAX.

In the fourth quarter of 2019 the state unemployment rate was 4.4%, marginally lower than the 4.5% level of a year ago. My most recent economic forecast suggests that statewide job growth in 2020 will rise 2.2%, with a total of 76,300 new jobs created.

HOME SALES

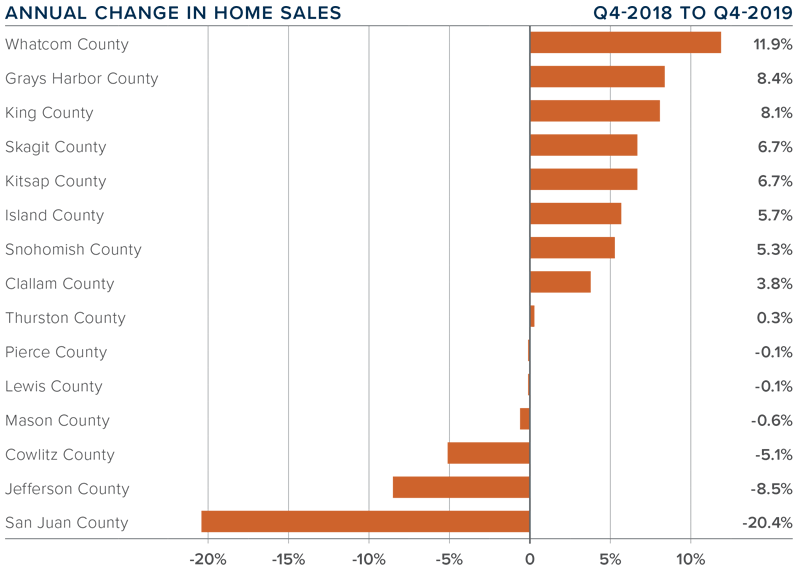

- There were 18,322 home sales registered during the final quarter of 2019, representing an impressive increase of 4.7% from the same period in 2018.

- Readers may remember that listing activity spiked in the summer of 2018 but could not be sustained, with the average number of listings continuing to fall. Year-over-year, the number of homes for sale in Western Washington dropped 31.7%.

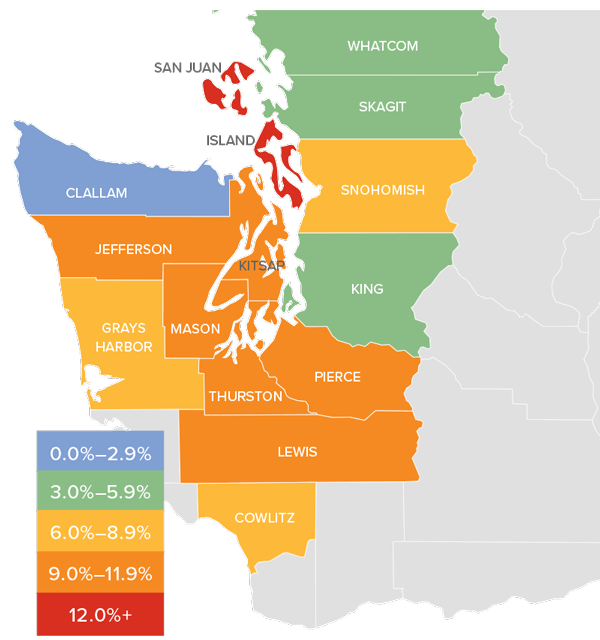

- Compared to the fourth quarter of 2018, sales rose in nine counties and dropped in six. The greatest growth was in Whatcom County. San Juan County had significant declines, but this is a very small market which makes it prone to extreme swings.

- Pending home sales — a barometer for future closings — dropped 31% between the third and fourth quarters of 2019, suggesting that we may well see a dip in the number of closed sales in the first quarter of 2020.

HOME PRICES

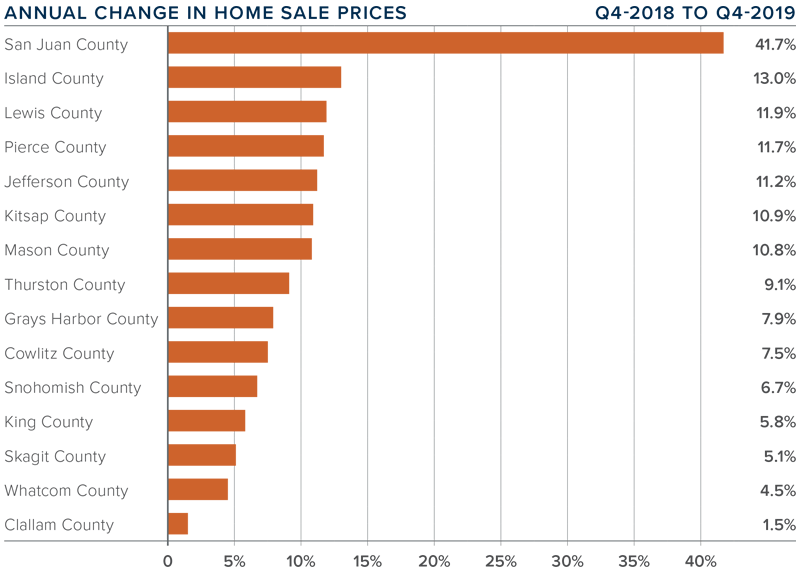

- Home price growth in Western Washington spiked during fourth quarter, with average prices 8.3% higher than a year ago. The average sale price in Western Washington was $526,564, 0.7% higher than in the third quarter of 2019.

- It’s worth noting that above-average price growth is happening in markets some distance from the primary job centers. I strongly feel this is due to affordability issues, which are forcing buyers farther out.

- Compared to the same period a year ago, price growth was strongest in San Juan County, where home prices were up 41.7%. Six additional counties also saw double-digit price increases.

- Home prices were higher in every county contained in this report. I expect this trend to continue in 2020, but we may see a softening in the pace of growth in some of the more expensive urban areas.

DAYS ON MARKET

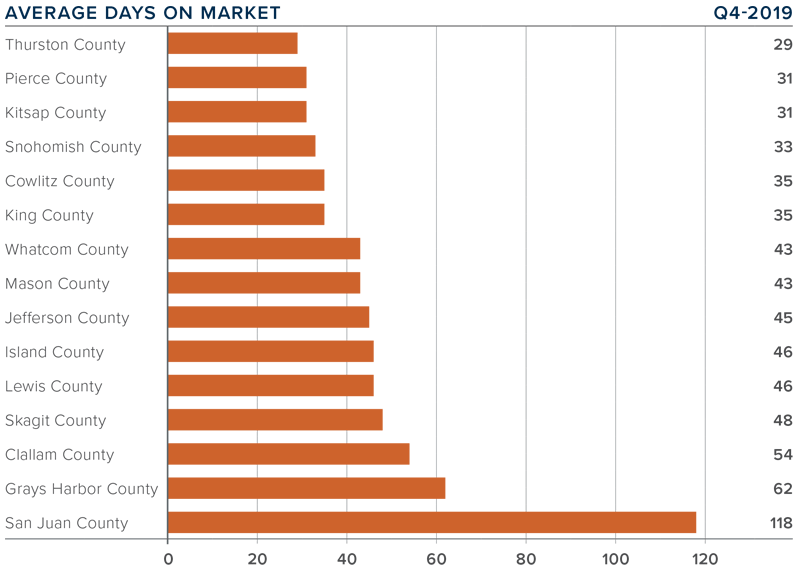

- The average number of days it took to sell a home dropped four days compared to the third quarter of 2019.

- For the second quarter in a row, Thurston County was the tightest market in Western Washington, with homes taking an average of 29 days to sell. In nine counties, the length of time it took to sell a home dropped compared to the same period a year ago. Market time rose in four counties and two were unchanged.

- Across the entire region, it took an average of 47 days to sell a home in the fourth quarter. This was up nine days over the third quarter of this year.

- Market time remains below the long-term average across the region, a trend that will likely continue until we see more inventory come to market — possibly as we move through the spring.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The housing market ended the year on a high note, with transactions and prices picking up steam. I believe the uncertainty of 2018 (when we saw significant inventory enter the market) has passed and home buyers are back in the market. Unfortunately, buyers’ desire for more inventory is not being met and I do not see any significant increase in listing activity on the horizon. As such, I have moved the needle more in favor of home sellers.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

This post originally appeared on the Windermere.com Blog.

Office: 425.455.5300

Direct: 425.890.3318

Email: davidhogan@windermere.com

Windermere Real Estate Bellevue

700 112th Ave NE #100, Bellevue, WA 98004